Exhibit 11

TRANSLATION FROM THE FRENCH VERSION FOR INFORMATION PURPOSES ONLY

This offer and this draft joint offer document remain subject to approval by the French stock market authority

PROPOSED PUBLIC BUY-OUT OFFER

FOLLOWED BY A SQUEEZE-OUT

RELATING TO THE SHARES AND BONDS CONVERTIBLE INTO

NEW SHARES OR EXCHANGEABLE FOR EXISTING SHARES

(OCEANES) OF THE COMPANY

INITIATED BY

NOKIA CORPORATION

PRESENTED BY

DRAFT JOINT OFFER DOCUMENT (PROJET DE NOTE D’INFORMATION CONJOINTE)

PREPARED BY NOKIA CORPORATION AND ALCATEL LUCENT

PRICE OF THE OFFER:

3.50 euros per Alcatel Lucent share

4.51 euros per Alcatel Lucent 2019 OCEANE

4.50 euros per Alcatel Lucent 2020 OCEANE

DURATION OF THE OFFER:

10 trading days

This draft joint offer document was prepared and filed with the French stock market authority (Autorité des marchés financiers) (the “AMF”) on September 6, 2016, in accordance with the provisions of Articles 231-13, 231-16, 231-18 and 231-19 of the general regulation of the AMF (the “AMF General Regulation”).

IMPORTANT NOTICE

Subject to the clearance decision of the AMF, following the public buy-out offer which is the subject of this draft joint offer document, the squeeze-out procedure provided by Article L. 433-4, II of the Monetary and Financial Code will be implemented. The Alcatel Lucent shares and OCEANEs not tendered into the public buy-out offer will be transferred on the trading day following the expiration date of the public buy-out offer to Nokia, in consideration for a compensation of 3.50 euros per Alcatel Lucent share, 4.51 euros per Alcatel Lucent 2019 OCEANE and 4.50 euros per Alcatel Lucent 2020 OCEANE, net of all costs.

THIS OFFER AND THIS DRAFT JOINT OFFER DOCUMENT

REMAIN SUBJECT TO APPROVAL BY THE AMF

This draft joint offer document is available on the websites of the AMF (www.amf-france.org), Nokia (www.nokia.com) and Alcatel Lucent (www5.alcatel-lucent.com). Copies of this draft joint offer document may be obtained free of charge from:

| Nokia Karaportti 3 FI-02610 Espoo Finland |

Alcatel Lucent 148-152, route de la Reine 92100 Boulogne-Billancourt France |

Société Générale CORI/COR/FRA 75886 Paris Cedex 18 France |

In accordance with Article 231-28 of the AMF General Regulation, the information documents relating, in particular, to the legal, financial and accounting characteristics of Nokia and Alcatel Lucent will be filed with the AMF and made available to the public, no later than the day preceding the opening of the public buy-out offer, on the same terms.

TABLE OF CONTENTS

| 1. PRESENTATION OF THE OFFER |

1 | |

| 1.1 Context of the Offer |

2 | |

| 1.1.1 History of the holding of Nokia in the Company |

4 | |

| 1.1.2 Thresholds crossing declarations |

4 | |

| 1.1.3 Alcatel Lucent’s share capital ownership |

5 | |

| 1.2 Reasons for the offer |

5 | |

| 1.3 Intentions of Nokia over the next twelve months |

5 | |

| 1.3.1 Industrial, commercial and financial strategy and policy |

6 | |

| 1.3.2 Employment |

7 | |

| 1.3.3 Commitments made in the context of the French foreign investments approval |

8 | |

| 1.3.4 Composition of the corporate and management bodies of Nokia and Alcatel Lucent |

10 | |

| 1.3.5 Benefits of the Offer for the Company, its shareholders and its holders of OCEANEs |

10 | |

| 1.3.6 Contemplated synergies – anticipated economic profits |

11 | |

| 1.3.7 Merger – legal reorganization |

11 | |

| 1.3.8 Dividend distribution policy |

11 | |

| 1.4 Agreements that could have a material impact on the assessment or outcome of the Offer |

11 | |

| 2. CHARACTERISTICS OF THE OFFER |

11 | |

| 2.1 Terms of the Offer |

11 | |

| 2.2 Number and nature of the Securities concerned by the Offer |

12 | |

| 2.3 Offer procedure |

12 | |

| 2.4 Situation of the holders of OCEANEs, holders of Stock Options, beneficiaries of Performance Shares, and Shares held in a company mutual fund |

13 | |

| 2.4.1 Position of OCEANEs holders |

13 | |

| 2.4.2 Position of the holders of Stock Options |

15 | |

| 2.4.3 Position of the beneficiaries of Performance Shares |

17 | |

| 2.4.4 Liquidity mechanism |

18 | |

| 2.4.5 Position of Shares held by a company mutual fund (fonds commun de placement d’entreprise) |

20 | |

| 2.5 Procedure for tendering into the Public Buy-Out Offer |

20 | |

| 2.6 Squeeze-out, delisting from Euronext Paris and Deregistration |

21 | |

| 2.7 Indicative timetable of the offer |

22 | |

| 2.8 Financing and costs of the offer |

23 | |

| 2.8.1 Costs linked with the Offer |

23 | |

| 2.8.2 Financing of the Offer |

23 | |

| 2.9 Restrictions concerning the Offer outside of France |

23 | |

| 2.9.1 General |

23 | |

| 2.9.2 Important additional information for U.S. holders of Securities |

23 | |

| 2.10 Tax regime applicable to the Offer in France |

24 | |

| 2.10.1 The Offer relating to the Shares |

24 | |

| 2.10.2 The Offer relating to the OCEANEs |

30 | |

| 3. INFORMATION REGARDING ALCATEL LUCENT |

31 | |

| 3.1 Alcatel Lucent’s share capital structure |

31 | |

| 3.2 Restrictions to the exercise of voting rights and share transfers |

31 | |

| 3.2.1 Notification of threshold crossing and identification of shareholders |

31 | |

| 3.2.2 Share transfer |

32 | |

| 3.2.3 Agreements providing for preferential Share transfer or purchase provisions on at least 0.5% of the share capital or voting rights of Alcatel Lucent (Article L. 233-11 of the French Commercial Code) |

32 |

i

| 3.3 Direct or indirect holdings in the Company’s share capital disclosed pursuant to the crossing of a threshold or a transaction on securities |

32 | |

| 3.4 List of holders of any securities carrying special control rights and a description of such rights |

32 | |

| 3.5 Control mechanisms provided for in an eventual employee participation scheme, when control rights are not exercised by the latter |

32 | |

| 3.6 Agreements between shareholders known to the Company and that may entail restrictions on share transfers and the exercise of voting rights |

33 | |

| 3.7 Rules applicable to the appointment and replacement of members of the board of directors, as well as to the amendment of the articles of association of the Company |

33 | |

| 3.7.1 Rules applicable to the appointment and replacement of members of the board of directors |

33 | |

| 3.7.2 Rules applicable to amendments of the articles of association of the Company |

33 | |

| 3.8 Powers of the board of directors relating in particular to the issuance and repurchase of securities |

34 | |

| 3.9 Agreements entered into by the company which will be amended or terminated in the event of a change of control of Alcatel Lucent |

34 | |

| 3.10 Agreements providing for indemnity to the Alcatel Lucent Chief Executive Officer, to the members of the board of directors or to employees if they resign or are dismissed without just or serious grounds or if their employment ceases because of a tender offer |

34 | |

| 4. ASSESSMENT OF THE PRICE OF THE OFFER |

34 | |

| 4.1 Appraisal of the Offer price for the Shares |

35 | |

| 4.1.1 Financials |

35 | |

| 4.1.2 Enterprise value to equity value bridge |

36 | |

| 4.1.3 Number of Shares retained |

37 | |

| 4.1.4 Methodologies retained |

37 | |

| 4.1.5 Methodologies used for informational purpose |

41 | |

| 4.1.6 Excluded methodologies |

41 | |

| 4.1.7 Summary of the elements provided to appraise the Offer price for Shares |

42 | |

| 4.2 Appraisal of the Offer price for the OCEANEs |

42 | |

| 4.2.1 Key terms of the OCEANEs |

42 | |

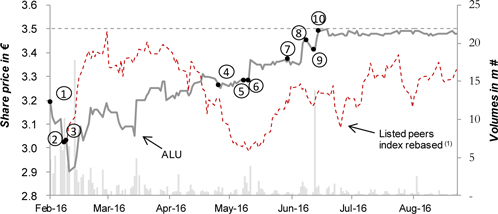

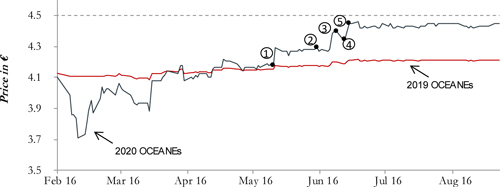

| 4.2.2 OCEANE’s market price |

43 | |

| 4.2.3 OCEANEs’ acquisition price |

43 | |

| 4.2.4 Theoretical Value |

43 | |

| 4.2.5 Summary of the elements provided to assess the Offer prices for OCEANEs |

44 | |

| 5. REPORT OF THE INDEPENDENT EXPERT (ARTICLE 261-1, I AND II OF THE AMF GENERAL REGULATION) |

44 | |

| 6. REASONED OPINION OF THE BOARD OF DIRECTORS OF ALCATEL LUCENT |

45 | |

| 7. INFORMATION RELATING TO NOKIA AND ALCATEL LUCENT MADE AVAILABLE TO THE PUBLIC |

50 | |

| 8. PERSONS RESPONSIBLE FOR THE DRAFT JOINT OFFER DOCUMENT |

50 | |

| 8.1 For the presenting bank |

50 | |

| 8.2 For Nokia |

50 | |

| 8.3 For Alcatel Lucent |

50 |

ii

| 1. | PRESENTATION OF THE OFFER |

Pursuant to Section III of Book II, specifically Articles 236-3 and 237-1 of the AMF General Regulation, Nokia Corporation, a company organized and existing under the laws of Finland, registered in the Finnish Trade Register under number 0112038-9, with registered office at Karaportti 3, FI-02610 Espoo, Finland (“Nokia” or the “Offeror”), whose shares are admitted to trading on Nasdaq OMX Helsinki Ltd. (“Nasdaq Helsinki”) and on Compartment A of the regulated market of Euronext Paris (“Euronext Paris”) under ISIN code FI0009000681, and, in the form of American Depositary Shares (“ADSs”), on the New York Stock Exchange (“NYSE”), irrevocably proposes to the shareholders and holders of OCEANES of Alcatel Lucent, a public limited company (société anonyme) with a share capital of 176 966 565.70 euros as of August 31 2016, divided into 3 539 331 314 shares with a nominal value of 0.05 euro each, having its registered office at 148/152 route de la Reine, 92100 Boulogne-Billancourt, France, registered in the Nanterre Trade and Companies Register under number 542 019 096 (“Alcatel Lucent” or the “Company”), to purchase pursuant to this public buy-out offer (the “Public Buy-Out Offer”), which will be immediately followed by a squeeze-out procedure (the “Squeeze-Out”, and together with the Public Buy-Out Offer, the “Offer”):

| • | all shares of the Company listed on Euronext Paris (Compartment A) under ISIN code FR0000130007, symbol “ALU” (the “Shares”) at the unit price of 3.50 euros; |

| • | all 2019 OCEANEs (as defined in Section 2.4.1) of the Company listed on Euronext Paris under ISIN code FR0011948306, symbol “YALU1”, at the unit price of 4.51 euros; |

| • | all 2020 OCEANEs (as defined in Section 2.4.1) of the Company listed on Euronext Paris under ISIN code FR0011948314, symbol “YALU2”, at the unit price of 4.50 euros. |

The 2019 OCEANEs and the 2020 OCEANEs are collectively referred to as the “OCEANEs” and, together with the Shares, the “Securities”.

As of the date of this draft joint offer document, Nokia directly holds 3 373 845 309 Shares representing 95.32% of the share capital and 95.25% of the voting rights of Alcatel Lucent on the basis of a total number of 3 539 331 314 Shares and 3 541 996 443 voting rights of Alcatel Lucent calculated pursuant to Article 223-11 of the AMF General Regulation, as well as 82 608 794 of the 2019 OCEANEs representing 92.46% of the outstanding 2019 OCEANEs, and 22 233 534 of the 2020 OCEANEs representing 81.66% of the outstanding 2020 OCEANEs. Nokia also holds 95.15% of the Alcatel Lucent Shares on a fully diluted basis.

The Offer targets:

| • | all Shares not held by the Offeror: |

| • | which are already issued, being, to the knowledge of the Offeror at the date of this draft joint offer document, 165 486 005 Shares, representing 4.68% of the share capital and 4.67% of the theoretical voting rights of the Company; |

| • | which may be issued before the expiration date of the Public Buy-Out Offer following (i) the conversion of OCEANEs (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 11 731 972 Shares), (ii) the exercise of Alcatel Lucent stock options not covered by a liquidity agreement (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 12 876 556 Shares) or (iii) the vesting of Alcatel Lucent performance shares not covered by a liquidity agreement (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximal number of 345 842 Shares); |

1

the sum of the foregoing being equal to, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 190 440 375 Shares;

| • | all of the 2019 OCEANEs not held by the Offeror, being, to the knowledge of the Offeror at the date of this draft joint offer document, 6 739 521 2019 OCEANEs; and |

| • | all of the 2020 OCEANEs not held by the Offeror, being, to the knowledge of the Offeror at the date of this draft joint offer document, 4 992 451 2020 OCEANEs. |

The Alcatel Lucent Performance Shares (as defined in Section 2.4.3 of this draft joint offer document) which remain unvested at the expiration date of the Public Buy-Out Offer are not targeted by the Offer. However, the Performance Shares vested but subject to a holding period and not covered by a liquidity agreement at the expiration date of the Public Buy-Out Offer are targeted by the Offer. These Performance Shares cannot be tendered into the Public Buy-Out Offer, due to the holding obligation applicable to their beneficiary and unless such holding obligation is removed pursuant to the applicable legal and statutory provisions (disability or death of the beneficiary). These Performance Shares will be subject to the Squeeze-Out that will follow the Public Buy-Out Offer, in accordance with Articles 237-1 and 237-10 of the AMF General Regulation.

To the Offeror’s knowledge, there are no other rights, equity securities or financial instruments that may give access, immediately or in the future, to the share capital or voting rights of the Company.

In the Squeeze-Out, the Shares and OCEANEs not then held by Nokia will be transferred to Nokia in exchange for a compensation which will be the same as the unit price of the Public Buy-Out Offer, i.e. 3.50 euros per Share, 4.51 euros per 2019 OCEANE and 4.50 euros per 2020 OCEANE (each net of all costs).

In accordance with the provisions of Article 231-13 of the AMF General Regulation, Société Générale, as presenting bank of the Offer, guarantees the content and the irrevocable nature of the commitments undertaken by the Offeror in the context of the Offer.

| 1.1 | CONTEXT OF THE OFFER |

| 1.1.1 | History of the holding of Nokia in the Company |

| 1.1.1.1 | Public exchange offer |

On April 15, 2015, Nokia and Alcatel Lucent entered into a Memorandum of Understanding, as amended on October 28, 2015 (the “Memorandum of Understanding”), pursuant to which Nokia filed a public exchange offer for all Alcatel Lucent Shares and all OCEANEs with a maturity date of July 1, 2018 (the “2018 OCEANEs”), all 2019 OCEANEs and all 2020 OCEANEs (the “Public Exchange Offer”). The material events that led to the signing of the Memorandum of Understanding and a summary of the terms of the Memorandum of Understanding are set out in Nokia’s offer document relating to the Public Exchange Offer which received visa No. 15-573 of the AMF and in Alcatel Lucent’s response document relating to the Public Exchange Offer which received visa No. 15-574 of the AMF.

Pursuant to Articles 232-1 et seq. of the AMF General Regulation, Nokia filed with the AMF the proposed Public Exchange Offer on October 29, 2015. The exchange ratios offered in the Public Exchange Offer were 0.5500 Nokia share per one Share, 0.6930 Nokia share per one 2018 OCEANE, 0.7040 Nokia share per one 2019 OCEANE and 0.7040 Nokia share per one 2020 OCEANE. On November 12, 2015, the AMF declared that the Public Exchange Offer complied with applicable laws and regulations and delivered its visa on Nokia’s offer document relating to the Public Exchange Offer and on Alcatel Lucent’s response document relating to the Public Exchange Offer.

2

A parallel public exchange offer was made in the United States, on financial conditions identical to those of the Public Exchange Offer, to all holders of ADSs representing Alcatel Lucent Shares then listed on the NYSE, wherever they were located, as well as to all U.S. holders of Alcatel Lucent Shares, 2018 OCEANEs, 2019 OCEANEs and 2020 OCEANEs (The “U.S. Public Exchange Offer”).

The Public Exchange Offer and the U.S. Public Exchange Offer were opened between November 18, 2015, and December 23, 2015 (inclusive), and reopened between January 14, 2016, and February 3, 2016 (inclusive). In the context of these offers, Nokia acquired 2 795 977 950 Shares (including Alcatel Lucent Shares represented by ADSs), 211 579 445 of the 2018 OCEANEs, 57 852 372 of the 2019 OCEANEs and 72 783 038 of the 2020 OCEANEs.

Following the Public Exchange Offer and the U.S. Public Exchange Offer, Nokia held 2 795 977 950 Shares representing, after adjustment of the monthly information of Alcatel Lucent on February 15, 2016 (per the press release of the Company issued on February 22, 2016), 90.34% of the share capital and 90.25% of the voting rights of the Company, 211 579 445 of the 2018 OCEANEs representing 99.62% of the outstanding 2018 OCEANEs, 57 852 372 of the 2019 OCEANEs representing 37.18% of the outstanding 2019 OCEANEs and 72 783 038 of the 2020 OCEANEs representing 68.17% of the outstanding 2020 OCEANEs.

| 1.1.1.2 | Conversion of OCEANEs following the Public Exchange Offer |

Following the Public Exchange Offer, on the date of settlement-delivery of the reopened offer, Nokia converted all of the OCEANEs it held.

After this conversion, Nokia held 3 229 781 374 Shares representing, after adjustment of the monthly information of Alcatel Lucent on February 15, 2016 (per the press release of the Company issued on February 22, 2016), 91.53% of the share capital and 91.45% of the voting rights of Alcatel Lucent.

| 1.1.1.3 | Acquisition of Alcatel Lucent Shares and OCEANEs after the Public Exchange Offer |

On February 18, 2016, Nokia acquired 11 820 932 Shares through a privately negotiated transaction, at the exchange ratio of the Public Exchange Offer (i.e., 0.5500 Nokia share per one Alcatel Lucent Share).

On March 16, 2016, Nokia entered into an agreement with JPMorgan Chase Bank, N.A., acting as depositary in the Alcatel Lucent American depositary receipts (“ADRs”) program, relating to the acquisition of all the Alcatel Lucent Shares underlying the remaining outstanding ADRs after termination of the ADR program, which occurred on April 25, 2016. Pursuant to this agreement, Nokia acquired 107 775 949 Shares on May 9, 2016, at the exchange ratio of the Public Exchange Offer (i.e., 0.5500 Nokia share per one Alcatel Lucent Share).

On May 12, 2016, Nokia acquired 72 994 133 of the 2019 OCEANEs and 19 943 533 of the 2020 OCEANEs through a privately negotiated transaction, in consideration for the payment of 4.51 euros per 2019 OCEANE and 4.50 euros per 2020 OCEANE.

Between May 9, 2016 and May 31, 2016, Nokia acquired a total of 74 784 Shares at the exchange ratio of the Public Exchange Offer (i.e., 0.5500 Nokia share per one Alcatel Lucent Share), pursuant to liquidity agreements entered into with Alcatel Lucent stock option holders.

Also, between June 1, 2016 and June 14, 2016, Nokia acquired 24 392 270 Shares, 9 614 661 of the 2019 OCEANEs and 2 290 001 of the 2020 OCEANEs, through privately negotiated transactions, in consideration for the payment of 3.50 euros per Share, 4.51 euros per 2019 OCEANE and 4.50 euros per 2020 OCEANE.

3

As of the date of this joint draft offer document, Nokia directly holds 3 373 845 309 Shares, 82 608 794 of the 2019 OCEANEs and 22 233 534 of the 2020 OCEANEs, representing 95.32% of the share capital and 95.25% of the theoretical voting rights of Alcatel Lucent, and 95.15% of the Shares on a fully diluted basis.

| 1.1.2 | Thresholds crossing declarations |

In accordance with the provisions of Articles L. 233-7 et seq. of the French Commercial Code, the following thresholds crossing declarations have been submitted by Nokia to the AMF and to the Company following the transactions mentioned in Section 1.1.1 of this draft joint offer document:

| Date of |

AMF notice | Declaration of intent |

Type | Thresholds | Nature of the transaction | |||||

| June 16, 2016 |

No. 216C1399 | No | ì | 95% | Acquisition of Alcatel Lucent Shares off market | |||||

| February 17, 2016 |

No. 216C0516 | No | ì | 90% | Acquisition of Alcatel Lucent Shares during the reopened offer period of the Public Exchange Offer | |||||

| January 12, 2016 |

No. 216C0121 | Yes | ì | 5%, 10%, 15%, 20%, 25%, 30%, 33 1⁄3%, 50%, 66 2⁄3% |

Acquisition of Alcatel Lucent Shares during the initial offer period of the Public Exchange Offer |

| 1.1.3 | Alcatel Lucent’s share capital ownership |

To the Offeror’s knowledge, and on the basis of the information communicated by the Company, the share capital and voting rights of Alcatel Lucent are held as follows as of August 31, 2016:

| Shareholders |

Capital on the basis of outstanding shares as of August 31, 2016 |

THEORETICAL voting rights on the basis of outstanding shares as of August 31, 2016(1) |

Voting rights EXERCISABLE AT SHAREHOLDERS’ MEETING on the basis of outstanding shares as of August 31, 2016(2) |

|||||||||||||||||||||||||

| Number of shares |

% of capital |

Double voting rights |

Total number of voting rights |

% of voting rights |

Total number of voting rights |

% of voting rights |

||||||||||||||||||||||

| Nokia Corporation |

3 373 845 309 | 95.32 | % | — | 3 373 845 309 | 95.25 | % | 3 373 845 309 | 95.25 | % | ||||||||||||||||||

| Treasury shares |

— | — | — | — | — | — | — | |||||||||||||||||||||

| Public |

165 486 005 | 4.68 | % | 2 665 129 | 168 151 134 | 4.75 | % | 168 151 134 | 4.75 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

3 539 331 314 | 100 | % | 2 665 129 | 3 541 996 443 | 100 | % | 3 541 996 443 | 100 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (1) | Theoretical voting rights calculated pursuant to Article 223-11 of the AMF General Regulation. The number of theoretical voting rights is calculated by taking into account the treasury shares held by the Company and its subsidiaries, which do not have voting rights. |

| (2) | The number of voting rights exercisable at Shareholders’ Meeting is calculated without taking into account the Shares which have no voting rights. |

4

| 1.2 | REASONS FOR THE OFFER |

Since Nokia holds more than 95% of Shares on a fully diluted basis and of the Alcatel Lucent voting rights, it filed with the AMF this proposed Public Buy-Out Offer which will be followed by a Squeeze-Out relating to all of the Shares and OCEANEs not held by Nokia, in accordance with the provisions of Article 236-3 of the AMF General Regulation.

The Offer is being done to consolidate Nokia’s ownership of Alcatel Lucent and acquire 100% of Alcatel Lucent to complete the combination of the businesses of the two companies. The Offer will then allow Alcatel Lucent and its subsidiaries to be fully integrated in the Nokia group (together, the “Nokia Group”).

The implementation of the Squeeze-Out will eliminate Alcatel Lucent’s regulatory and administrative obligations related to the admission of its Securities to trading on Euronext Paris and will consequently reduce the related costs.

Minority shareholders and holders of Alcatel Lucent OCEANEs will obtain full and immediate liquidity for their Securities.

The Offeror has appointed Société Générale to carry out a valuation of the Shares and OCEANEs, which is summarized in Section 4 of this draft joint offer document.

Furthermore, pursuant to the provisions of Article 261-1, I and II of the AMF General Regulation, Alcatel Lucent appointed Accuracy, represented by Messrs. Bruno Husson and Henri Philippe, as independent expert (the “Independent Expert”) responsible for assessing the financial conditions of the Offer. The report of the Independent Expert (the “Independent Expert Report”), which concludes that the price proposed to the shareholders and holders of OCEANEs in the context of the Public Buy-Out Offer is fair, is reproduced in full in Section 5 of this draft joint offer document.

| 1.3 | INTENTIONS OF NOKIA OVER THE NEXT TWELVE MONTHS |

| 1.3.1 | Industrial, commercial and financial strategy and policy |

The implementation of the Offer does not alter the industrial, commercial and financial strategy of Nokia toward Alcatel Lucent described in Nokia’s offer document relating to the Public Exchange Offer.

The proposed Offer is a continuation of the Public Exchange Offer which permitted the combination between Nokia and Alcatel Lucent and the creation of an innovation leader in next generation technology and services for an IP-connected world. The headquarters of the Nokia Group is in Finland with strategic business locations and major R&D centers in France, as well as in Germany, the United States and China. The strategic goal of the combination was to create a combined company with an end-to-end portfolio scope and scale and leading global positions across next generation network technologies and services.

Nokia believes that Nokia and Alcatel Lucent have highly complementary assets, technologies and portfolios, bringing together fixed and mobile broadband, IP routing, core networks, cloud applications and services, as well as complementary geographical exposures, with particular strength in the United States, China, Europe and Asia-Pacific.

The combination is expected to create access to an expanded addressable market. In addition, together the companies are expected to be better equipped to meet the increasingly complex needs of customers globally given industry trends, including global telecommunications consolidation and convergence; expansion to quad-play offerings and delivering seamless experiences across multiple screens and applications; timing of the 5G investment cycle; and transition to the cloud.

5

The Nokia Group also utilizes its unique innovation capabilities and is expected to be in a position to accelerate development of future technologies including 5G, IP and software-defined networking, the cloud and analytics.

In addition, Nokia expects to maintain its long-term financial objective of returning to an investment grade credit rating and intends to manage the capital structure of the Nokia Group accordingly, including by retaining adequate gross and net cash positions and by proactively reducing indebtedness. Nokia intends to optimize its capital structure, including maintaining an efficient capital structure and continuing annual dividend payments following completion of the Offer.

The Nokia Group targets approximately EUR 1.2 billion of total annual cost savings to be achieved in full year 2018 compared to the combined non-IFRS operating costs of Nokia and Alcatel Lucent for full year 2015, excluding Nokia Technologies.

| 1.3.2 | Employment |

The commitments of Nokia in France relating to employment remain materially the same as those described in Nokia’s offer document relating to the Public Exchange Offer:

| • | Follow the Shift Plan commitments regarding the level of employment in France, for a period of at least two (2) years after the consummation of the Public Exchange Offer. The base comprises Alcatel Lucent France/International (ALUI) operational heads (excluding branches), Bell Labs France, RFS (Radio Frequency Systems) and excluding Alcatel-Lucent Submarine Networks (ASN) and Eu factory (Landing point of the reference perimeter is 4 200 Headcount and excluding RFS unit). Nokia will maintain resources from its French operations throughout the reference period to support its customers in France; |

| • | Strengthen the operations and activity levels for the long term at the two major technology sites of Villarceaux (Essonne) and Lannion (Cotes d’Armor) following the consummation of the Public Exchange Offer, with a focus on augmenting existing activities, functions, and advanced research work; |

| • | Increase significantly and sustainably the R&D presence in France scaling up 5G, IP network management platforms and cyber-security with employment evolving from 2 000 people to 2 500 people including the recruiting of at least 300 newly graduated talents over the coming three (3) years. The R&D employment level will be maintained for a period of at least four (4) years after the consummation of the Public Exchange Offer; |

| • | Localize in France worldwide technology centers of expertise following the consummation of the transaction, including in the areas of: |

| • | 5G R&D to anchor France in the future of wireless activities for the Nokia Group. France will be equipped with a full 5G innovation engine which will encompass research activities with Bell Labs, development activities as well as end to end platforms and trial networks; |

| • | IP management platforms; |

| • | Cyber Security (research, product development and platforms) while continuing to leverage the partnership established by Alcatel Lucent with Thalès; |

| • | Bell Labs; and |

| • | Wireless Transmission; |

6

| • | A major worldwide corporate organization in charge of strategic innovation including networks research and Bell Labs will be led from France and will comprise key staff members; |

| • | Maintain some operations and activities at operational hubs located in France and providing services to other locations in the world following the consummation of the Public Exchange Offer, including in the areas of: |

| • | Local support services; |

| • | Local pre- and post-sales resources for France and selected European & African countries; |

| • | Take all necessary measures to find sustainable solutions for the French employees who could be impacted by the rationalization of corporate activities between Nokia and Alcatel Lucent. |

| 1.3.3 | Commitments made in the context of the French foreign investments approval |

The commitments of Nokia made in the context of the foreign investments approval in France relating to the Public Exchange Offer remain the same as those described in Nokia’s offer document relating to the Public Exchange Offer, as summarized below.

Alcatel Lucent is represented by three board members in the combined company. Nokia shares have been admitted to trading on the regulated market of Euronext Paris. The combined company will establish or keep the adequate legal entities in France and comply with French regulations related to sensitive contracts.

Nokia expects to benefit from becoming a deeply embedded part of France, tapping into and helping develop the technology ecosystem of the country. Nokia will invest further in the digital innovation ecosystem in France following the completion of the transaction, primarily through the establishment of a long-term investment fund in the range of EUR 100 million. This fund will mainly target the Internet of Things, cyber-security and software platform enablers for next generation networks.

Nokia intends to support the development of the overall telecom ecosystem in France and to ensure continuity of Alcatel Lucent’s current initiatives. This involves playing an active role in the government’s “Industry of the Future” program, funding academic tuition, programs and chairs, situating technology experts within France (such as within Bell Labs France), and continuing Alcatel Lucent’s involvement in major initiatives such as Pôles de compétitivité Systematic, Cap Digital, and Images and Réseaux. Nokia will also develop three industrial platforms and networks prototypes in France within the fields of 5G, Industrial Internet / Internet of Things connectivity and cyber-security.

Following the completion of the combination, Nokia, which will remain headquartered in Finland, intends to leverage the combined strengths of the companies’ strategic business locations and major R&D centers in other countries, including Finland, Germany, the United States and China.

Nokia has committed, upon completion of the combination, to providing regular updates to the French government as the integration of the two companies progresses.

7

| 1.3.4 | Composition of the corporate and management bodies of Nokia and Alcatel Lucent |

| 1.3.4.1 | Corporate and management bodies of Nokia |

Nokia’s board of directors consists of eight members. The members of the board of directors of Nokia who were previously directors of Alcatel Lucent are Louis R. Hughes, Jean C. Monty and Olivier Piou, with Mr. Piou serving as vice chairman of the Nokia board of directors.

As of the date of this draft joint offer document, the board of directors of Nokia, for a term ending at the close of the Annual General Meeting in 2017, is comprised of the following members:

| • | Risto Siilasmaa (chairman); |

| • | Olivier Piou (vice chairman); |

| • | Bruce Brown; |

| • | Louis R. Hughes; |

| • | Jean C. Monty; |

| • | Elisabeth Nelson; |

| • | Carla Smits-Nusteling; and |

| • | Kari Stadigh. |

Effective from September 1, 2016, the Nokia Group Leadership Team, led by Rajeev Suri, is comprised of the following twelve members (the President and Chief Executive Officer, four business group leaders and seven unit leaders):

| • | Rajeev Suri, President and Chief Executive Officer; |

| • | Samih Elhage, President of Mobile Networks; |

| • | Federico Guillén, President of Fixed Networks; |

| • | Basil Alwan, President of IP/Optical Networks; |

| • | Bhaskar Gorti, President of Applications & Analytics; |

| • | Timo Ihamuotila, Chief Financial Officer; |

| • | Hans-Jürgen Bill, Chief Human Resources Officer; |

| • | Kathrin Buvac, Chief Strategy Officer; |

| • | Ashish Chowdhary, Chief Customer Operations Officer; |

| • | Barry French, Chief Marketing Officer; |

| • | Marc Rouanne, Chief Innovation & Operating Officer; and |

| • | Maria Varsellona, Chief Legal Officer. |

8

Ramzi Haidamus, former President of Nokia Technologies and member of the Nokia Group Leadership Team, stepped down from the Nokia Group Leadership Team effective from September 1, 2016. Brad Rodriguez, currently head of strategy and business development in Nokia Technologies, assumed the role of acting President of Nokia Technologies, while the company search for a permanent successor is on-going.

It is not anticipated that the composition of the corporate and management bodies of Nokia will be modified as a result of the Offer.

| 1.3.4.2 | Corporate and management bodies of Alcatel Lucent |

| (a) | Board of directors |

On January 8, 2016, following the success of Nokia’s Public Exchange Offer, the composition of the board of directors of Alcatel Lucent was modified to reflect the new ownership structure of the Company.

Risto Siilasmaa, Rajeev Suri, Timo Ihamuotila, Maria Varsellona and Samih Elhage have been coopted to the board of directors of Alcatel Lucent. These cooptations have been ratified by the shareholders of Alcatel Lucent at the 2016 Annual General Meeting held on June 21, 2016. In addition, Marc Rouanne was appointed as a director at that general meeting.

The mandate of chairman of the board of directors and Chief Executive Officer of Philippe Camus, who was confirmed in his position following the success of the Public Exchange Offer, ended with effect as of June 21, 2016. The board of directors, at its meeting of June 21, 2016, resolved to segregate the positions of Chairman of the board of directors and Chief Executive Officer. Upon the recommendation of the Corporate Governance and Nominating Committee, as of June 21, 2016, Marc Rouanne was appointed Chairman of the board of directors and Olivier Durand was appointed Chief Executive Officer of the Company.

As of the date of this draft joint offer document, the board of directors of Alcatel Lucent is comprised of the following members:

| • | Marc Rouanne (chairman); |

| • | Carla Cico (independent director); |

| • | Jean-Cyril Spinetta (independent director); |

| • | Sylvia Summers (independent director); |

| • | Samih Elhage; |

| • | Timo Ihamuotila; |

| • | Risto Siilasmaa; |

| • | Rajeev Suri; and |

| • | Maria Varsellona. |

The board of directors of Alcatel Lucent also includes two board observers allowing the presence of employees of the Company or of a company of the Alcatel Lucent Group during meetings of the board of directors:

| • | Laurent du Mouza; |

| • | Gilles Le Dissez. |

9

The composition of the board of directors of Alcatel Lucent is expected to be modified to reflect the shareholding of the Company as a result of the Offer.

| (b) | Management |

As of the date of this draft joint offer document, the Chief Executive Officer of the Company is Olivier Durand.

As of June 21, 2016, the Management committee is comprised of the following members:

| • | Olivier Durand, Chief Executive Officer; |

| • | Barbara Larsen, General Counsel; |

| • | Philippe Guillemot, Chief Operating Officer; |

| • | Loïc Le Grouiec, Human Resources; and |

| • | Franck Mauroy, interim Chief Financial Officer. |

| 1.3.5 | Benefits of the Offer for the Company, its shareholders and its holders of OCEANEs |

The Offer will allow the minority shareholders and holders of OCEANEs of Alcatel Lucent to obtain full and immediate liquidity for their Securities.

As a result of the delisting of the Company Securities from Euronext Paris, the Offer eliminates Alcatel Lucent’s regulatory and administrative obligations related to the admission to trading of its Securities on Euronext Paris and therefore reduces the related costs; it being specified that the Offeror’s shares are admitted to trading on the Nasdaq Helsinki, on Euronext Paris and, in the form of ADSs, on the NYSE.

The elements of assessment of the price of the Offer are specified in Section 4 of this draft joint offer document.

| 1.3.6 | Contemplated synergies – anticipated economic profits |

This proposed Offer is made in the context of the combination of Nokia and Alcatel Lucent initiated through the Public Exchange Offer. Upon announcing the combination on April 15, 2015, Nokia announced that the combined company would target approximately EUR 900 million of annual operating cost synergies to be achieved on a full year basis in 2019. On October 29, 2015 Nokia accelerated the target of approximately EUR 900 million of annual operating cost synergies to be achieved on a full year basis in 2018, relative to the combined non-IFRS results of Nokia and Alcatel-Lucent for full year 2015. In conjunction with the publication of Nokia’s first quarter 2016 results on May 10, 2016, Nokia updated its annual operating cost synergy target to above EUR 900 million of net operating cost synergies to be achieved in full year 2018.

In conjunction with the publication of Nokia’s second quarter and half year 2016 results on August 4, 2016, Nokia transformed its previously announced annual operating cost synergy target to an overall cost savings program, which also includes other cost savings measures that are not related to the combination of Nokia and Alcatel Lucent. Nokia currently targets approximately EUR 1.2 billion of total annual cost savings to be achieved in full year 2018 compared to the combined non-IFRS operating costs of Nokia and Alcatel Lucent for full year 2015, excluding Nokia Technologies.

10

Under this cost savings program, restructuring and associated charges are expected to total approximately EUR 1.2 billion, of which approximately EUR 600 million was recorded in Q2 2016.

Related restructuring and associated cash outflows are expected to total approximately EUR 1.65 billion, which includes the approximately EUR 450 million balance of restructuring and associated cash outflows that were provisioned for but not yet paid as of the beginning of Q2 2016, related to previous Nokia and Alcatel-Lucent restructuring and cost savings programs. In addition to the above amounts, Nokia’s overall charges and cash outflows will include amounts related to network equipment swaps. The charges related to network equipment swaps will be recorded as non-IFRS exclusions, and therefore will not affect Nokia’s non-IFRS operating profit.

| 1.3.7 | Merger – legal reorganization |

As of the date of this draft joint offer document, a merger of the Company with the Offeror or any company of its group is not under consideration.

| 1.3.8 | Dividend distribution policy |

The dividend distribution policy of Alcatel Lucent will continue to be determined by the managing bodies of the Company in regards to the distribution capabilities, financial situation and needs of the Company.

Alcatel Lucent has not distributed any dividends in the last eight fiscal years.

| 1.4 | AGREEMENTS THAT COULD HAVE A MATERIAL IMPACT ON THE ASSESSMENT OR OUTCOME OF THE OFFER |

Other than the Liquidity Mechanism covering the Stock-Options and the Performance Shares described in Section 2.4.4 of this draft joint offer document, to the knowledge of Nokia, no other agreements exist that may have a material impact on the assessment of the Offer or its outcome.

| 2. | CHARACTERISTICS OF THE OFFER |

| 2.1 | TERMS OF THE OFFER |

Pursuant to the provisions of Articles 231-13, 236-3 and 237-1 of the AMF General Regulation, on September 6, 2016, Société Générale, acting as presenting bank, on behalf of the Offeror, filed with the AMF both the proposed Offer in the form of a public buy-out offer followed by a squeeze-out (offre publique de retrait suivi d’un retrait obligatoire) relating to the Alcatel Lucent Shares and OCEANEs not held by Nokia and the draft joint offer document.

The Offeror irrevocably undertakes to purchase from Alcatel Lucent’s shareholders and holders of OCEANEs all Shares and OCEANEs targeted by the Offer that are tendered into the Public Buy-Out Offer, at a price of 3.50 euros per Share, 4.51 euros per 2019 OCEANE, and 4.50 euros per 2020 OCEANE, during a 10 trading days period.

The Shares and OCEANEs which are not tendered into the Public Buy-Out Offer will be transferred to the Offeror in the context of the Squeeze-Out on the trading day following the expiration date of the Public Buy-Out Offer, in consideration for 3.50 euros per Share, 4.51 euros per 2019 OCEANE, and 4.50 euros per 2020 OCEANE, net of all costs.

In accordance with Article 231-13 of the AMF General Regulation, Société Générale guarantees the content and the irrevocable nature of the commitments undertaken by the Offeror in the context of the Offer.

11

| 2.2 | NUMBER AND NATURE OF THE SECURITIES CONCERNED BY THE OFFER |

As of the date of this draft joint offer document, Nokia directly holds 3 373 845 309 Shares representing 95.32% of the share capital and 95.25% of the voting rights of Alcatel Lucent, as well as 82 608 794 of the 2019 OCEANEs representing 92.46% of the outstanding 2019 OCEANEs, and 22 233 534 of the 2020 OCEANEs representing 81.66% of the outstanding 2020 OCEANEs. Nokia also holds 95.15% of the Alcatel Lucent Shares on a fully diluted basis.

The Offer targets:

| • | all Shares not held by the Offeror: |

| • | which are already issued, being, to the knowledge of the Offeror at the date of this draft joint offer document, 165 486 005 Shares, representing 4.68% of the share capital and 4.67% of the theoretical voting rights of the Company; |

| • | which may be issued before the expiration date of the Public Buy-Out Offer following (i) the conversion of OCEANEs (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 11 731 972 Shares), (ii) the exercise of Alcatel Lucent stock options not covered by a liquidity agreement (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 12 876 556 Shares) or (iii) the vesting of Alcatel Lucent performance shares not covered by a liquidity agreement (being, to the knowledge of the Offeror at the date of this draft joint offer document, a maximal number of 345 842 Shares); |

the sum of the foregoing being equal to, to the knowledge of the Offeror at the date of this draft joint offer document, a maximum number of 190 440 375 Shares;

| • | all of the 2019 OCEANEs not held by the Offeror, being, to the knowledge of the Offeror at the date of this draft joint offer document, 6 739 521 2019 OCEANEs; and |

| • | all of the 2020 OCEANEs not held by the Offeror, being, to the knowledge of the Offeror at the date of this draft joint offer document, 4 992 451 2020 OCEANEs. |

The Alcatel Lucent Performance Shares (as defined in Section 2.4.3 of this draft joint offer document) which remain unvested at the expiration date of the Public Buy-Out Offer are not targeted by the Offer. However, the Performance Shares vested but subject to a holding period and not covered by a liquidity agreement at the expiration date of the Public Buy-Out Offer are targeted by the Offer. These Performance Shares cannot be tendered into the Public Buy-Out Offer, due to the holding obligation applicable to their beneficiary and unless and unless such holding obligation is removed pursuant to the applicable legal and statutory provisions (disability or death of the beneficiary). However, these Performance Shares will be subject to the Squeeze-Out that will follow the Public Buy-Out Offer, in accordance with Articles 237-1 and 237-10 of the AMF General Regulation.

To the Offeror’s knowledge, there are no other rights, equity securities or financial instruments that may give access, immediately or in the future, to the share capital or voting rights of the Company.

| 2.3 | OFFER PROCEDURE |

The proposed Offer has been filed with the AMF on September 6, 2016. A notice of filing will be published by the AMF on its website (www.amf-france.org).

12

In accordance with the provisions of Article 231-16 of the AMF General Regulation, this draft joint offer document is made available free of charge to the public at the registered offices of the Offeror and the Company, and at Société Générale, and has been published on the websites of the AMF (www.amf-france.org), the Offeror (www.nokia.com) and Alcatel Lucent (www5.alcatel-lucent.com). In addition, a press release relating to the terms of the Offer was issued on September 6, 2016.

This Offer and this draft joint offer document remain subject to approval by the AMF.

After having assessed that the Offer complies with the applicable legal and regulatory provisions, the AMF will publish a duly reasoned clearance decision on its website. This clearance decision will be deemed to constitute a visa of the draft joint offer document.

The joint offer document having received the clearance from the AMF and the “other information” documents relating, in particular, to the legal, financial and accounting characteristics of the Offeror and the Company, will be made available to the public free of charge, pursuant to Article 231-28 of the AMF General Regulation, no later than on the day preceding the opening of the Public Buy-Out Offer, at the registered office of the Offeror, the Company and at Société Générale. The same will also be available on the websites of the AMF (www.amf-france.org), the Offeror (www.nokia.com) and the Company (www5.alcatel-lucent.com).

Pursuant to Articles 231-27 and 231-28 of the AMF General Regulation, a press release indicating the means by which these documents are made available will be published by the Offeror and the Company at the latest on the second trading day following the clearance decision of the AMF regarding the joint offer document, and at the latest on the day preceding the opening of the Public Buy-Out Offer regarding the “other information” documents relating, in particular, to the legal, financial and accounting characteristics of the Offeror and the Company.

Prior to the opening of the Public Buy-Out Offer, the AMF will publish a notice of opening and timetable of the Offer, and Euronext Paris will publish a notice announcing the timetable and the main characteristics of the Public Buy-Out Offer, as well as the condition of implementation of the Squeeze-Out, including the date of its implementation.

| 2.4 | SITUATION OF THE HOLDERS OF OCEANES, HOLDERS OF STOCK OPTIONS, BENEFICIARIES OF PERFORMANCE SHARES, AND SHARES HELD IN A COMPANY MUTUAL FUND |

| 2.4.1 | Position of OCEANEs holders |

On June 10, 2014, Alcatel Lucent issued 167 500 000 OCEANEs with a maturity date of January 30, 2019 (the “2019 OCEANEs”). The terms and conditions of the 2019 OCEANEs are set out in the securities note included in the prospectus that received the visa No. 14-254 of the AMF on June 2, 2014, established for the issuance of the 2019 OCEANEs and 2020 OCEANEs. The 2019 OCEANEs, which have a par value of 4.11 euros, with an annual interest rate of 0%, and a maturity date of January 30, 2019, are convertible or exchangeable at any time after July 20, 2014, and provide a right to one new or existing Alcatel Lucent Share for every one 2019 OCEANE, subject to the adjustments provided for by the prospectus and pursuant to the conditions of the said prospectus. To the Offeror’s knowledge, 89 348 315 of the 2019 OCEANEs are outstanding at the date of this draft joint offer document, of which 82 608 794 are directly held by the Offeror, representing 94.46% of the outstanding 2019 OCEANEs.

On June 10, 2014, Alcatel Lucent issued 114 499 995 OCEANEs with a maturity date of January 30, 2020 (the “2020 OCEANEs”). The terms and conditions of the 2020 OCEANEs are set out in the securities note included in the prospectus that received the visa No. 14-254 of the AMF on June 2, 2014, established for the issuance of the 2019 OCEANEs and 2020 OCEANEs. The 2020 OCEANEs, which have a par value of 4.02 euros, with an annual interest rate of 0.125%, and a

13

maturity date of January 30, 2020, are convertible or exchangeable at any time after July 20, 2014, and provide a right to one new or existing Alcatel Lucent Share for every one 2020 OCEANE, subject to the adjustments provided for by the prospectus and pursuant to the conditions of the said prospectus. To the Offeror’s knowledge, 27 225 985 of the 2020 OCEANEs are outstanding at the date of this draft joint offer document, of which 22 233 534 are directly held by the Offeror, representing 81.66% of the outstanding 2020 OCEANEs.

| 2.4.1.1 | OCEANEs tendered into the Public Buy-Out Offer |

Holders of OCEANEs may tender their OCEANEs into the Public Buy-Out Offer in accordance with the procedures set out in Section 2.5 of this draft joint offer document.

| 2.4.1.2 | Exercise of the OCEANEs conversion/exchange right |

According to the terms of the prospectus relating to the issuance of the OCEANEs, holders of OCEANEs may convert/exchange the OCEANEs they hold into/against Alcatel Lucent Shares. In such case, the conversion/exchange ratio applicable to the OCEANEs will not be adjusted as a result of the Offer.

The exercise date of the request to exercise the OCEANEs conversion/exchange right must, in any case, be prior to September 30, 2016 at 5 p.m., Paris time, in order for the Shares to be delivered prior to the expiration date of the Public Buy-Out Offer or, as the case may be, the Squeeze-Out.

If a request to exercise the OCEANEs conversion/exchange right occurs after September 30, 2016 at 5 p.m., Paris time, no Shares will be delivered and the OCEANEs will be covered by the Squeeze-Out.

| 2.4.1.3 | Early redemption resulting from a Change of Control |

In accordance with the terms of the OCEANEs, with the Public Exchange Offer having resulted in a change of control of Alcatel Lucent, any holder of OCEANEs has, at his or her sole discretion, been able to request the early redemption in cash of the OCEANEs held at par plus, as applicable, accrued interest from the date interest was last paid, pursuant to the terms of the prospectus relating to the issuance of the OCEANEs.

Upon completion of the initial period of the Public Exchange Offer, the Company informed the holders of OCEANEs of a change of control by means of a notice issued by the Company on January 22, 2016, and published on its website (www5.alcatel-lucent.com). A notice was issued by Euronext Paris on the same day.

Holders of OCEANEs could request early redemption of their OCEANEs between January 22, 2016 and February 12, 2016. The date set for early redemption was February 26, 2016. The redemption price was 1.81170 euros for the 2018 OCEANEs, 4.11 euros for the 2019 OCEANEs and 4.02037 euros for the 2020 OCEANEs.

| 2.4.1.4 | Early redemption of the OCEANEs representing less than 15% of the issued OCEANEs of their series |

Since less than 15% of the issued 2018 OCEANEs remained outstanding, pursuant to the terms of the 2018 OCEANEs, on March 21, 2016, the Company redeemed at par value plus accrued interests from the date interest was last paid to the date set for the early redemption all outstanding 2018 OCEANEs.

The early redemption price was 1.80 euro plus accrued interests, i.e., a total of 1.81672 euros per 2018 OCEANE.

14

Holders of the 2018 OCEANEs could exercise their rights to the allocation of Shares until the 7th working day (inclusive) prior to the date set for early redemption, i.e., until March 10, 2016.

| 2.4.2 | Position of the holders of Stock Options |

The Company has granted stock options (the “Stock Options”) pursuant to several plans during 2007, 2008, 2009, 2010, 2011, 2012 and 2013, the main features of which are set out on pp. 164 et seq. of the 2015 reference document (Document de Référence) of the Company filed with the AMF on April 28, 2016 under No. D. 16-0427 and available on the websites of the Company (www5.alcatel-lucent.com) and the AMF (www.amf-france.org). For the 2014 financial year, it was agreed in the Memorandum of Understanding entered into between Nokia and Alcatel Lucent on April 15, 2015, that the allocation of Stock Options would be replaced by the allocation of Company Shares under conditions similar to the ones described in Section 2.4.2.2 of this draft joint offer document.

To the knowledge of the Offeror, as of August 31 2016, there were 13 076 307 Stock Options outstanding, out of which (i) 199 751 Stock Options are exercisable and covered by a liquidity agreement (as described in Section 2.4.4 of this draft joint offer document) which are therefore not targeted by the Offer, (ii) 12 782 240 Stock Options are exercisable and the Shares resulting from their exercise are immediately transferable and may be tendered into the Public Buy-Out Offer, according to the procedure set forth in Section 2.5 of this draft joint offer document and (iii) 94 316 Stock Options are unvested and not exercisable unless such vesting is accelerated (in particular in case of disability or death of the beneficiary) in which case the Stock Options will be exercisable and the Shares resulting from their exercise will be immediately transferable and may be tendered into the Public Buy-Out Offer, according to the procedure set forth in Section 2.5 of this draft joint offer document. It is contemplated that the Stock Options referred to in (ii) and (iii) be converted into Stock Option Units (see Section 2.4.2.3 of this draft joint offer document).

| 2.4.2.1 | Acceleration mechanism in the context of the Public Exchange Offer |

In the context of the Public Exchange Offer, Alcatel Lucent offered to holders of Stock Options granted before April 15, 2015, the execution date of the Memorandum of Understanding, an option to accelerate their rights to exercise their Stock Options subject to certain conditions, including that the Public Exchange Offer is successful, that the beneficiaries satisfy the presence condition on the last day of the initial offer period of the Public Exchange Offer (December 23, 2015) and that they accept that all of their Stock Options covered by the acceleration as well as all the vested Stock Options (except, as the case may be, those which were subject to a tax lock-up period provided by French or Belgian law) would be exercised and that their Shares resulting from the exercise of these Stock Options would be sold on the open market no later than two trading days prior to the last day of reopened offer period of the Public Exchange Offer.

However, the beneficiaries were released from their commitment to exercise the Stock Options and sell the resulting Shares when the sum of the exercise price of these Stock Options and the costs and expenses relating to this exercise and to the sale of the Shares resulting from such exercise was higher than the sale price of their Shares. These beneficiaries had irrevocably accepted the terms and conditions of the liquidity agreement described in Section 2.4.4.1 of this draft joint offer document with respect to these unexercised Stock Options. Likewise, these beneficiaries had irrevocably accepted the terms and conditions of the liquidity agreement described in Section 2.4.4.1 of this draft joint offer document with respect to the Stock Options subject to a tax lock-up period provided by French law or Belgian law, unless they opted for an acceleration agreement that covers such Stock Options.

In certain jurisdictions, the mechanisms described above were adapted to applicable legal, regulatory or other local constraints.

15

With respect to the beneficiaries of Stock Options who did not accept the acceleration, the terms and conditions of their Stock Options remained unchanged, including the presence conditions. Some of these beneficiaries may also benefit from a liquidity mechanism, under certain conditions and insofar as applicable regulations allowed it (see Section 2.4.4.1 of this draft joint offer document).

| 2.4.2.2 | Replacement plan offered to the beneficiaries of the 2014 stock-options plan in the context of the Public Exchange Offer |

Alcatel Lucent had considered granting (but did not grant) a stock-options plan for the financial year 2014. In lieu of this stock-options plan, Alcatel Lucent offered to the persons who would be beneficiaries of such plan unrestricted Shares according to the following ratio: one Share for each two stock-options. Such grant was subject to the Public Exchange Offer being successful, the beneficiaries satisfying the presence condition on the last day of the initial offer period of the Public Exchange Offer (December 23, 2015) and accepting that their Shares thus received would be sold on the market no later than two trading days before the last day of the reopened offer period of the Public Exchange Offer.

In certain jurisdictions, the mechanisms described above were adapted to the applicable legal, regulatory or other local constraints.

| 2.4.2.3 | Conversion of the remaining Stock Options plans in a stock-option units plan |

On September 13, 2016, a proposal will be made to the Alcatel Lucent shareholders at a general meeting to decide the conversion in instruments settled in cash of the Stock Options not yet exercised and not covered by a liquidity agreement (the “Stock Option Units”).

The terms and conditions of these Stock Option Units will be embedded in a Stock Option Units plan which will be adopted by the Company’s board of directors upon delegation from the Company shareholders’ general meeting.

This Stock Option Units plan will provide that the grant date, the vesting period, the exercise price and the exercise period for such Stock Option Units will remain as set out in the Alcatel Lucent Stock Options plan for the Stock Options that are being replaced.

The acquisition of all the rights attached to those Stock Option Units will remain subject to a condition of presence, i.e., the beneficiaries of Stock Option Units shall maintain their position as salaried employees of the Nokia Group, at the expiration date of this acquisition period.

Following the acquisition of the Stock Option Units, the beneficiaries will be able to exercise them at any time during an eight-year period from the granting date of the Alcatel Lucent Stock Options that these Stock Option Units will replace, at the exercise price of the replaced Alcatel Lucent Stock Options. Upon exercise of these Stock Option Units, the beneficiaries will receive, for each Stock Option Unit exercised, an amount in cash equal to the difference between (i) the value of one Alcatel Lucent Share and (ii) the exercise price of the Stock Option Unit increased by any taxes and/or fees applicable to the exercise of the Stock Option Unit.

For purposes of the preceding paragraph, the value of one Share will be equal to the stock price of a Nokia share on Nasdaq Helsinki at the closing of business of the trading day preceding the exercise date multiplied by the exchange ratio of the Public Exchange Offer as adjusted following the decision of Nokia’s shareholders’ general annual meeting held on June 16, 2016 to pay a special dividend of 0.10 euro per Nokia share (i.e., an exchange ratio equal to 0.5610 Nokia share for one Alcatel Lucent Share) and subject to further adjustments in accordance with the terms of the Stock Option Unit Plan.

In certain jurisdictions, the mechanism described above may be adapted to legal, regulatory or any other applicable constraints.

16

| 2.4.3 | Position of the beneficiaries of Performance Shares |

The Company has allocated performance shares (the “Performance Shares”) free of charge within the framework of several plans during 2008, 2009, 2010, 2011, 2012, 2013, 2014, and 2015, the main features of which are set out on pp. 158 et seq. of the 2015 reference document (Document de Référence) of the Company filed with the AMF on April 28, 2016 under No. D. 16-0427, available on the websites of the Company (www5.alcatel-lucent.com) and the AMF (www.amf-france.org).

To the knowledge of the Offeror, as of August 31 2016, there were 9 770 752 unvested Performance Shares (all granted in the context of the plan of September 15, 2014 or July 29, 2015), out of which (i) 9 424 910 unvested Performance Shares are covered by a liquidity agreement (as described in Section 2.4.4 of this draft joint offer document) which are therefore not targeted by the Offer, and (ii) 345 842 unvested Performance Shares are not covered by a liquidity agreement and are targeted by the Offer in the event such vesting is accelerated, in which case the Shares resulting from their vesting may be tendered into the Public Buy-Out Offer, according to the procedure set forth in Section 2.5 of this draft joint offer document or, in the event such Shares are subject to a holding period, will be subject to the Squeeze-Out, according to the procedure set forth in Section 2.6 of this draft joint offer document. In addition, 95 137 vested Performance Shares that remain subject to a holding period which is not expected to expire at the expected expiration date of the Public Buy-Out Offer or the implementation of the Squeeze-Out (all granted in the context of the plan of July 12, 2013) are targeted by the Offer.

| 2.4.3.1 | Waiver mechanism in the context of the Public Exchange Offer |

In the context of the Public Exchange Offer, Alcatel Lucent offered to holders of the unvested Performance Shares granted before April 15, 2015, the execution date of the Memorandum of Understanding, to waive their rights under the Performance Shares plans in exchange for an indemnity payable in Shares free from any performance conditions, but subject to the conditions that the Public Exchange Offer is successful, that the beneficiaries satisfy the presence condition on the last day of the initial offer period of the Public Exchange Offer (December 23, 2015) and that they accept that their Shares thus received would be sold on the market no later than 2 trading days prior to the last day of the reopened offer period of the Public Exchange Offer.

In certain jurisdictions, the mechanism described above has been adapted to legal, regulatory or any other applicable constraints.

The terms and conditions of the Performance Shares of the beneficiaries who did not accept such waiver remained unchanged, including the presence or performance requirement. However, the Alcatel Lucent board of directors decided, regarding the performance conditions, to modify them in case of Reduced Liquidity (as defined in section 2.4.4.1 of this draft joint offer document), in order to replace the stock market price of Shares by the stock market price of Nokia shares as reference stock market price and to adjust the representative reference sample of Alcatel Lucent peers by withdrawing Nokia from it. As from February 12, 2015, at least one of the Reduced Liquidity conditions was fulfilled – the Offeror holding more than 85% of the Shares of the Company – and thus, the revised performance conditions are now applicable.

Some beneficiaries benefited from a liquidity mechanism, under certain conditions and subject to applicable regulations (see Section 2.4.4.1 of this draft joint offer document).

With respect to the Performance Shares subject to a vesting period and granted in 2015, the beneficiaries benefit from a liquidity mechanism (see Section 2.4.4.2 of this draft joint offer document).

17

| 2.4.3.2 | Acceleration in the context of this Offer |

On September 13, 2016, a proposal will be made to the Alcatel Lucent shareholders at a general meeting to authorize the board of directors to amend the September 15, 2014 Performance Shares plan to (i) remove the relevant performance condition, (ii) waive, as of August 31, 2016, the presence condition provided for in the rules of the Performance Shares Plan dated September 15, 2014 and (iii) replace the 4-year vesting period of these Performance Shares by a vesting period of two years followed by a 2-year holding period, in accordance with the provisions of the then applicable Article L. 225-197-1 of the French Commercial Code.

However, liquidity agreements were offered to beneficiaries of Performance Shares granted under the plan of September 15, 2014:

| • | a liquidity agreement was offered to French tax residents in the context of the Public Exchange Offer (see Section 2.4.4.1 of this draft joint offer document); and |

| • | more generally, a liquidity agreement was offered to beneficiaries of Performance Shares granted pursuant to the plan of September 15, 2014 before their acceleration in the context of the Offer (see Section 2.4.4.3 of this draft joint offer document). |

The acceleration will not apply to beneficiaries of Performance Shares who accepted these liquidity agreements.

Therefore, all the Performance Shares initially granted pursuant to the Performance Shares plan of September 15, 2014, with the exception of those covered by one of the liquidity agreements as described above, will be acquired by their beneficiaries on September 16, 2016 (instead of September 16, 2018).

The Performance Shares which will be acquired on September 16, 2016 cannot be tendered into the Public Buy-Out Offer, due to the holding obligation applicable to their beneficiary and unless such holding obligation is removed pursuant to the applicable legal and statutory provisions (disability or death of the beneficiary). Nonetheless, these Performance Shares will be subject to the Squeeze-Out, in accordance with Articles 237-1 and 237-10 of the AMF General Regulation.

| 2.4.4 | Liquidity mechanism |

| 2.4.4.1 | Liquidity offered in the context of the Public Exchange Offer to holders of Stock Options and beneficiaries of Performance Shares allocated before 2015 |

Pursuant to the Memorandum of Understanding, the Offeror proposed, between November 18, 2015 and December 23, 2015, a liquidity agreement to the French tax residents who, as a result of tax constraints, are beneficiaries of the following plans:

| • | Performance Shares Plan No. A0914RUROW and No. A0914RPROW of September 15, 2014; |

| • | Stock Options Plan No. A0812NHFR2 of August 13, 2012; |

| • | Stock Options Plan No. A0312COFR2, No. A0312CPFR2, and No. A0312NHFR2 of March 14, 2012. |

The liquidity agreement was also offered to Belgian tax residents who are beneficiaries of the Stock Options Plan No. A0713COBE2 dated July 12, 2013, provided that they opted for the taxation of these Stock Options and that they committed to holding these Stock Options in accordance with applicable law.

18

Pursuant to this liquidity agreement, in the event of (i) a delisting of the Company Shares, (ii) Nokia holding more than 85% of the Company Shares or (iii) an average daily trading volume of Company Shares on Euronext Paris falling below 5 million Shares for 20 consecutive trading days (a “Reduced Liquidity”), the Shares to be received by holders of Stock Options will be automatically exchanged for Nokia shares, or the cash equivalent of the market value of such Nokia shares. This liquidity agreement also provides that, in the event of Reduced Liquidity, the relevant Alcatel Lucent Performance Shares are to be automatically exchanged by Nokia for Nokia shares, or for the cash equivalent of the market value of such Nokia shares, shortly after expiration of the lock-up period.

As from February 12, 2015, at least one of the Reduced Liquidity conditions is fulfilled and thus, the revised performance conditions are now applicable.

The liquidity agreement relating to the Stock-Options plan n° A0812NHFR2 dated August 13, 2012, has already been executed and, between May 9, 2016 and May 31, 2016, Nokia acquired a total of 74 784 Shares according to the exchange ratio of the Public Exchange Offer (i.e., 0.5500 Nokia share per one Alcatel Lucent Share).

A liquidity agreement has also been entered into with the holders of non-vested and vested Stock-Options as described in Section 2.4.2.1 of the draft joint offer document. This liquidity agreement is also settled, as described above, either in Nokia shares or in a cash amount amounting to the market value of such Nokia shares. This liquidity agreement has been accepted by the beneficiaries at the same time they accepted the acceleration agreement.

In addition, a liquidity agreement has been offered between July 25, 2016 and August 26, 2016 to the holders of vested Stock Options not covered by the selling undertaking described in Section 2.4.2.1 of this draft joint offer document and for which the sum of the exercise price and the costs and expenses relating to this exercise and the sale of the Shares resulting from such exercise represented more than 90% of the Alcatel Lucent Share price as of the closing of the last day of the reopened offer period of the Public Exchange Offer on Euronext Paris. This liquidity agreement is also settled, as described above, either in Nokia shares or in a cash amount amounting to the market value of such Nokia shares.

The exchange ratio applicable to these liquidity agreements, which was the same as the exchange ratio of the Public Exchange Offer, i.e., 0.5500 Nokia share per one Alcatel Lucent Share, has been adjusted following the decision taken by the Annual General Meeting of Nokia held on June 16, 2016 to pay a special dividend of 0.10 euro per Nokia share. The exchange ratio is now of 0.5610 Nokia share per one Alcatel Lucent Share. The exchange ratio as adjusted is subject to further adjustments in the event of certain financial transactions performed by Nokia or Alcatel Lucent, in order for the holders of Stock Options and beneficiaries of Performance Shares to obtain the same value in Nokia shares or in cash that they would have obtained had such a transaction not taken place.

Due to legal, regulatory or any other applicable constraints in certain jurisdictions, the liquidity mechanism described above was not offered to certain beneficiaries of Options or only the cash settlement option is available.

| 2.4.4.2 | Liquidity offered to beneficiaries of Performance Shares granted in 2015 |

Pursuant to the Memorandum of Understanding, the Offeror has agreed to enter into a liquidity agreement with all beneficiaries of Performance Shares granted after April 15, 2015, pursuant to which, in case of a Reduced Liquidity at the date of expiration of the applicable vesting period, all Performance Shares will be automatically exchanged by Nokia for Nokia shares, or for the cash equivalent of the market value of such Nokia shares, shortly after expiration of such vesting period.

19

The exchange ratio applicable to the liquidity agreement, which was the same as the exchange ratio of the Public Exchange Offer, i.e., 0.5500 Nokia share per one Alcatel Lucent Share, has been adjusted following the decision taken by the Annual General Meeting of Nokia held on June 16, 2016 to pay a special dividend of 0.10 euro per Nokia share. The exchange ratio is now of 0.5610 Nokia share per one Alcatel Lucent Share. The exchange ratio is subject to further adjustments in the event of certain financial transactions of Nokia or Alcatel Lucent, in order for the beneficiaries of Performance Shares to obtain the same value in Nokia shares or in cash that they would have obtained had such a transaction not taken place.

In certain jurisdictions, only the cash settlement option is available in respect of those liquidity agreements due to legal, regulatory or any other applicable constraints.

| 2.4.4.3 | Liquidity offered to beneficiaries of Performance Shares granted in 2013 |

The Offeror has proposed to the beneficiaries of the Performance Shares granted pursuant to the Performance Shares plan of July 12, 2013 or the Performance Shares plan of September 15, 2014, which were not covered by a liquidity agreement offered to the beneficiaries within the context of the Public Exchange Offer (see Section 2.4.4.1 of this draft joint document), a liquidity agreement pursuant to which the Performance Shares held by the beneficiary will be automatically exchanged, at the end of the vesting period of the Performance Shares or, if applicable, at the end of the holding period of the Performance Shares, by Nokia, at Nokia’s discretion, for either:

| • | Nokia shares according to the exchange ratio of the Public Exchange Offer as adjusted following the decision of the Annual General Meeting of Nokia held on June 16, 2016 to pay a special dividend of 0.10 euro per Nokia share (i.e., an exchange ratio equal to 0.5610 Nokia share for one Alcatel Lucent Share) and subject to additional adjustments according to the terms of the liquidity agreement; or |

| • | an amount in cash equal to the market value of such Nokia shares. |

Due to legal, regulatory or any other applicable constraints, the liquidity mechanism described above was not offered to beneficiaries of Performance Shares located in Australia, Iran, Morocco and Saudi Arabia and only the cash settlement option is available in certain jurisdictions.

Holders of such Performance Shares had between September 2, 2016 and September 12, 2016 to accept this proposal.

The beneficiaries of the Performance Shares acquired pursuant to the Performance Shares Plan of July 12, 2013, subject to a holding period, informed the Company that they were not willing to enter into this liquidity agreement.

| 2.4.5 | Position of Shares held by a company mutual fund (fonds commun de placement d’entreprise) |

The mutual fund supervisory board (conseil de surveillance du Fonds Commun de Placement Actionnariat) of Alcatel Lucent (“FCP 2AL”), has tendered the Shares it held into the Public Exchange Offer. In January 2016, the FCP 2AL was renamed Fonds Commun de Placement Actionnariat Nokia (“FCP AN”). As of the date of this draft joint offer document, the FCP AN no longer holds any Shares.

| 2.5 | PROCEDURE FOR TENDERING INTO THE PUBLIC BUY-OUT OFFER |

The Public Buy-Out Offer will remain open for a 10 trading day period, in accordance with the provisions of Article 236-7 of the AMF General Regulation.

20

The Public Buy-Out Offer will be conducted through purchases on the market, the settlement-delivery being made as and when the orders are executed, within two trading days after each order is executed. The trading fees (i.e., the brokerage fees and the corresponding VAT) will remain the responsibility of the shareholders and holders of OCEANEs tendering their Securities, it being specified that the compensation offered in the context of the Squeeze-Out will be net of all costs. The member of the buying market, acting for the account of the Offeror, is Société Générale (member 4403).

The Securities tendered into the Public Buy-Out Offer must be freely transferable and free from all liens, pledges and all other security or encumbrance restricting the free transfer of their ownership. The Offeror reserves the right to disregard any Securities tendered into the Public Buy-Out Offer that do not meet this requirement.

The Company shareholders or the holders of OCEANEs whose Shares or OCEANEs are held through a financial intermediary (credit institutions, investment firms, etc.) and who wish to tender their Shares and/or OCEANEs into the Public Buy-Out Offer, on the conditions set forth in this draft joint offer document, must give an order to such financial intermediary to irrevocably sell their Securities in accordance with the form provided by such intermediary no later than on the expiration date of the Public Buy-Out Offer.